The Unearthing of “Something New” Has Historically Been a “New Risk”Impacting Solvency

By Joseph L. Petrelli

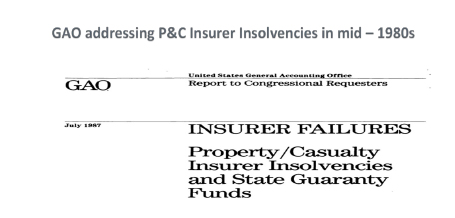

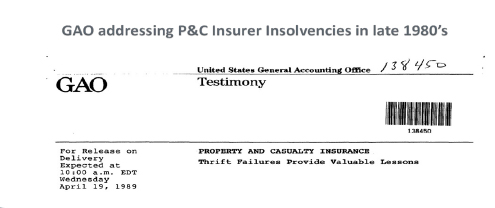

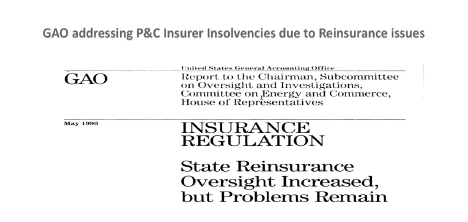

In 1989, Demotech Inc., became the first to review and rate independent, regional and specialty insurers. Well prior to our entry into insurer ratings, undetected phenomena had resulted in failures of insurers, often highly rated by other rating agencies. Once a “something new” was identified and isolated as the cause of the failures, the National Association of Insurance Commissioners, as well as the insurer rating agencies impacted by the “something new,” created reporting requirements to secure the information necessary to address the previously covert phenomenon in their review process. Examples of “somethings new” that resulted in carrier insolvencies were often documented in U.S. General Accounting Office reports:

None of the carrier failures referenced in the 1987, 1989, 1990 or 1992 General Accounting Office reports were insurers rated by Demotech. Each carrier referenced failed because “something new,” overt or covert, had been impacting its financial position, and no one, regulators, independent auditors, actuaries opining on loss and loss adjustment expense, even the carriers and the rating agencies following the carriers, had been able to identify in advance of the adverse financial impact. In each of these situations, hundreds of credentialed professionals focused on assessing the financial strength of the insurers were unable to detect the “something new” even though, in each situation summarized above, the “something new” was occurring in offices from coast to coast. In other words, “online” was not yet an option.

In December 2022, a Government Accountability Office report entitled “Third-Party Litigation Funding” was issued. The report noted that from 2017 to 2022, the third-party litigation funding dollars invested by the litigation funds that had been interviewed, doubled. This extensive, informative report provided insights on what, in 2022, was likely to be an emerging litigation financing sector.

Our research project was also initiated in 2022, the year of this GAO report; however, our research project, having the benefit of our postmortem and its discovery of the meteoric growth in new, litigated, annual claims over the period 2017 to 2022, anticipated that “technology” was involved in the dramatic increase in new, annual litigated claims. Demotech discovered this GAO report subsequent to our postmortem and research project, however, we are pleased to note that the preliminary results of Todd Kozikowski’s research included references to “litigation marketing” and “third-party litigation funding.” It was Demotech and Kozikowski who discerned that technology comprised the crux of the (then) covert online business model.

Prior to Demotech’s postmortem, research, and Kozikowski’s findings, authors and their reports discussing factors driving the increase in litigation frequency were unaware of the online nature of the business model that destroyed several carriers in Florida, including an insurer dual rated by ourselves and AM Best. This online business model remained covert as actuaries and independent auditors reviewed each of the failed carriers, multiple years prior to their year of liquidation.

In the summer of 2022, the immediate response of Kozikowski and myself was to educate the insurance industry to the “something new” that had destroyed carriers and adversely impacted numerous jurisdictions. The list of opportunities included the Bermuda Risk Summit, National Association of Insurance Commissioners, American Property Casualty Insurance Association, Risk and Insurance Management Society, Reinsurance Association of America, American Association of Insurance Services, Mutual Services Organization, National Association of Mutual Insurance Companies, and dozens of individual insurers and reinsurers. My testimony to the United States House of Representatives Committee on Financial Services hearing, “The Factors Influencing the High Cost of Insurance for Consumers,” Nov. 2, 2023, presented the findings and discussed the impact of the online business model of tech-enabled litigation instigation on the availability and affordability of insurance in other jurisdictions.

Throughout the history of insurance ratings, “something new” has been discovered periodically. As to the online business model of tech-enabled litigation instigation, although many have isolated separate components of the proximate causes destroying carriers and markets, only Demotech Inc., through its postmortem, research project, and Kozikowski’s findings has assembled the pieces of the puzzle.

Stay informed with the Demotech Difference Magazine.