The Decline of the Pension and the Rise of Pension Risk Transfer

By Mieley C. Cooke

Retirement professionals love their analogies. One of the more popular ones I’ve heard likens retirement planning to a marathon that begins on day one of employment. While that helps their clients visualize that they need to work toward retirement at a steady pace over a long period of time, I find it can imply that the course to retirement is smooth and predictable when it can often prove not. As post-retirement life expectancies continue to rise and inflation erodes the purchasing power of existing savings, the marathon’s course can have more hills, roadblocks, and hazards than originally anticipated.

Another common analogy likens retirement funding to a three-legged stool: one leg government programs (Social Security), one leg personal savings (401(k)s, 403(b)s, IRAs, and brokerage accounts), and one leg employer retirement plans (pensions). The three legs of the stool work together to support financial stability in retirement. I also have problems with this analogy, as a stool is only structurally sound if all three legs are contributing equally, and as we have seen, modern retirement plans often have little or no support from the final leg of the stool.

Declining Popularity of Pensions

Defined benefit (DB) pensions have fallen out of favor in lieu of defined contribution (DC) plans, in which employers commonly provide funds in the form of 401(k) or 403(b) contribution matches that give employees extra funds to save for their own retirement. While many people publicly outcry the loss of pensions (asking “Why are we putting the difficult responsibility of saving and investing in the hands of the average American instead of planning experts?”), I’d argue that both today’s system of largely 401(K}s and yesterday’s system of pensions both fail our poorest Americans who often lack access to these financial vehicles. According to the Social Security Bulletin, even near DB pensions’ peak popularity in 1980, the proportion of private wage and salary workers covered was only 38 percent1. As of 2023, less than 75 percent of civilian American workers have access to a 401(K) or other workplace retirement benefit according to the Bureau of Labor Statistics2. It’s clear that the biggest retirement issue we face — regardless of retirement system — is how we prepare the lowest earners in our society.

But why have pensions fallen out of favor? I can think of five key reasons that can be summarized as: pensions are expensive and employees desire them less.

- Market Risk: Pensions are invested in equities and bonds which can perform poorer than expected in pension liability calculations. This volatility can be difficult for companies to tolerate, as it leads to uncertainty in their financial statements unrelated to their core business performance. For public companies, this is particularly troublesome to explain to investors in quarterly earnings calls.

- Longevity Risk: Pension calculations depend heavily on how long workers and retirees are expected to live. Mortality improvement has led to higher-than-expected pension costs, frustrating companies unprepared for this risk.

- Rising PBGC Premiums: The Pension Benefit Guaranty Corporation is a federal agency that insures benefits promised under private-sector DB pensions. Companies are required to pay premiums to the PBGC. Recently, these premiums have gotten more expensive, which is putting considerable pressure on companies.

- Administrative Burden: Maintaining a pension plan is expensive and can lead to headaches that are a drain on management’s time. Data systems must be upgraded, pension participants have questions, and third-party administration solutions can be costly.

- Low Perceived Appeal: Current and potential employees often do not realize or understand the value of a pension plan, even if generous. It’s easier to sell a higher salary or more vacation days to potential or current employees as a reason to join or stay than explaining a complicated pension plan formula. Also, today’s workers are switching jobs more often, and value pension plans that reward longer tenures less than previous generations.

Enter: Pension Risk Transfer (PRT)

Given that pensions have fallen out of favor with many employers, PRT has risen in popularity as a way of removing pension liabilities from company balance sheets. It can take the form of offering lump-sum buyouts to plan participants or complicated transactions with insurance companies to cover future liabilities in exchange for money today. Insurers are often better positioned to manage longevity and asset-liability management risk than plan sponsors, allowing this to be a more cost-efficient approach.

Let’s look at an example. Take a midsize manufacturing company that began offering a pension plan in 1970. It has 2,000 blue-collar plan participants and 200 white-collar plan participants. Fifty percent of personnel were hired at least 20 years ago, and 50 percent of personnel were hired in the last five years due to a recent rapid expansion. The pension liability has continued to climb due to growing plan participation, volatile economic conditions, and rising PBGC per participant premiums. Additionally, the company is considering selling a stake in its ownership and is concerned about the perceived negative financial impact of its pension.

The company has decided to no longer offer a defined benefit plan to its new employees and will instead be offering a defined contribution plan. While this will help to limit defined benefit pension costs, the company is still worried about funding future pension liabilities for current and past employees. The company could approach a pension risk transfer broker to request bids for the cost to obtain a group payout annuity to cover the pension liability and remove this obligation from its financial statements. The broker would initiate the bidding process with life insurance companies interested in the business. The insurers would bid the minimum amount they’d be willing to accept to assume the responsibility of paying for all future pension benefit payments for the remainder of the participants’ lives. Often, the lowest price wins.

These transactions can be complex, with different participants carved out, varying arrangements for pension administration, and sophisticated funding structures. For example, this manufacturing company may choose to keep the liability of its older employees while looking to shift the risk of the employees hired in the last five years to an insurer. This is because the per person PBGC premiums are a lot more costly, as a percentage of pension benefits, for these newer employees than older employees. Differences in mortality between blue-collar and white-collar employees can also be a consideration.

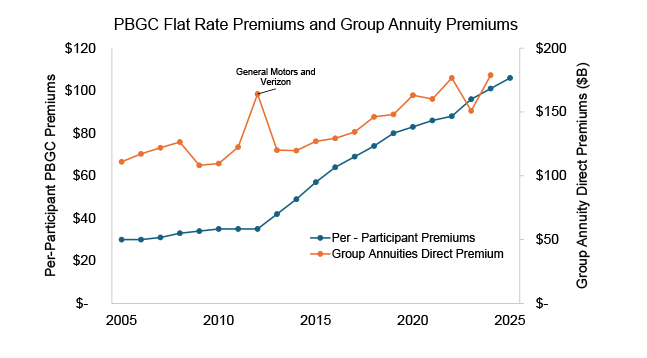

PBGC per-participant premiums have been climbing since 2013. This trend has coincided with high group annuity direct written premiums in life, accident & health company filings, Exhibit 1, Part 1. Much of the rise in group annuities can be attributed to higher PRT deals in recent years. Note that 2012 was a particularly large year for PRT driven by General Motors and Verizon’s deals with Prudential Financial that totaled nearly $40B.

PBGC per-participant premiums are sourced from the PBGC website, www.pbgc.gov, and premium data is sourced from S&P Global.

Concerns Surrounding PRT

While PRT can be an efficient way for a company to offload pension risk from their balance sheet, concerns have been raised that this has ultimately increased risk for plan participants and reduced their protections. When a pension plan is transferred to an insurance company, participants are no longer protected by ERISA, and their plans will no longer be backstopped by the PBGC. Regulation is instead the responsibility of individual states that monitor the insurance companies. While regulators seek to ensure that insurers are solvent and will be able to fulfill their promises, including those to pensioners, there is concern that complex reinsurance transactions, sometimes to offshore companies, can obfuscate risk from state regulators that wouldn’t otherwise exist in a pension plan managed by the original company. It’s also said that many transactions occur with companies or affiliates that are domiciled in jurisdictions with lighter regulation than other jurisdictions. Said simply, there’s worry that companies have only considered cost in these transactions and have neglected to sufficiently consider the financial stability of the bidding insurers.

In fact, several lawsuits have emerged that companies have violated their fiduciary duty to protect plan participants by engaging in these transactions.

Verizon Lawsuit

One notable lawsuit has been filed in the U.S. District Court for the Southern District of New York against Verizon Communications Inc. on behalf of the 56,000 participants in their defined benefit pension plans. The suit alleges that the PRT transaction between the company and Prudential Insurance Company of America and the reinsurer RGA violated fiduciary duties under ERISA. Rather than conducting thorough due diligence and considering the riskiness of the insurance carriers it transacted with, the suit claims that Verizon and its fiduciary, State Street Global Advisors, focused solely on price. Per suit language, this has transformed retirees “into certificate holders under risky group annuities that are no longer regulated by ERISA or insured by the [PBGC]”.

The plaintiffs are concerned that their pension is less secure, and their retirement finances could be in jeopardy if the group annuity purchased by their company is unable to perform. Benefits are no longer guaranteed by Verizon nor the PBGC, and retirees could be impacted if the insurance company faces insolvency.

Future Retirement Security

Pensioners have come to count on the promise that their monthly checks will be there for them in retirement. Whether their check is cashed from company reserves or an insurer’s shouldn’t particularly matter — unless the checks stop coming. As some consumer protections afforded under ERISA are not applicable when the pension liability has been transferred to an insurance company, the financial stability of life insurance companies is even more important. The rise in PRT transactions, particularly among private equity insurers, has prompted regulators to think about their current risk monitoring. While federal regulation is rapidly evolving under the current administration, prior efforts have been made to clarify the “factors relating to a potential annuity provider’s claims paying ability and creditworthiness” that a fiduciary should consider (Department of Labor’s Interpretive Bulletin 95-1). For extra protection, some plan sponsors have begun requesting their assets be held in a separate account rather than the insurer’s general account, even if this comes at a higher price.

For the rest of us who will statistically never experience a defined benefit plan, we still need to be better prepared for retirement. This may mean increasing financial and investment literacy and awareness, choosing employers with better retirement packages, or just simply saving more each paycheck. Of course, Social Security remaining intact and sufficiently funded will also help retirement preparedness … but that’s a discussion for another day.

Mieley Cooke provides both financial and business analysis for Demotech in the formulation and review of Financial Stability Ratings®, predominantly for life and health companies. Prior to joining Demotech in 2024, she worked as a life insurance actuary for a major carrier. Her experience is mostly in the life and annuity product space, including financial reporting and forecasting, pricing, and asset adequacy testing. Cooke has been a Fellow of the Society of Actuaries since 2022 and a Chartered Enterprise Risk Analyst since 2021. She is a member of the American Academy of Actuaries.

PBGC per-participant premiums have been climbing since 2013. This trend has coincided with high group annuity direct written premiums in life, accident & health company filings, Exhibit 1, Part 1. Much of the rise in group annuities can be attributed to higher PRT deals in recent years. Note that 2012 was a particularly large year for PRT, driven by General Motors and Verizon’s deals with Prudential Financial that totaled nearly $40B.

PBGC per-participant premiums were sourced from the PBGC website, www.pbgc.gov. Premium data was sourced from publically available NAIC statements sourced from S&P Global. Any conclusions based on the data are Demotech’s.

Stay informed with the Demotech Difference Magazine.