Demotech’s Research Project, Kozikowski’s Research, and a Speed Bump for the Online Business Model They Unearthed

Background

In April 2022, Demotech initiated a research project, undertaken by Todd Kozikowski, that unearthed the previously covert online business model that we called tech-enabled claim instigation or tech-enabled litigation instigation. This online business model had been covert circa 2017. I document below that its power to impact insurance markets is beyond anything previously seen, including the capability to destroy insurers, including American Capital Assurance Corporation, dual rated at a level by ourselves and AM Best, as well as markets being targeted .

This article outlines Demotech’s internal postmortem subsequent to the failures, tracks the development of the research project, and illustrates the power of the business model to transform claim settlement patterns in the insurance industry while it reinvents the legal profession. All of this explains why litigation funding is attracted to this business model. Finally, we concur with others on an effective response to this multi-faceted business model.

History

Several years ago, seven Florida-focused property insurers failed, including American Capital Assurance Corporation, which was dual-rated at the respective A level of Demotech Inc. and AM Best. The precipitous declines prior to failure triggered an internal postmortem by Demotech.This revealed that each insurer received unqualified “clean” independent audits from their inception to the year preceding failure. They also received determinations of reasonable provision as regards carried gross and net loss and loss adjustment expense reserves at each year-end prior to the year of failure.

Further, each of the unqualified independent audits and statements of actuarial opinion asserting a determination of reasonable provision that were issued implied that the carriers had adequately addressed the issues that (then) defined Florida’s residential property insurance marketplace at each year-end prior to failure. The issues addressed to the satisfaction of auditors, actuaries, and the State of Florida Office of Insurance Regulation in the decade prior to failure included but were not limited to:

• Sinkholes.

• One-way attorney fees.

• Assignment of benefits.

• Impact of the Joyce, Johnson, and Sebo judicial precedents on claim procedures.

• Disparate, disproportionate levels of property insurance litigation, as documented in studies prepared by the State of Florida Office of Insurance Regulation.

• Prolific billboards, TV, and radio advertising by plaintiff attorneys.

• Door-knocking and complimentary inspections by roofing companies.

• Dozens of tropical storms and hurricanes making landfall in Florida.

No carrier received a warning related to their level of litigation from their independent auditor nor the actuary opining on loss and LAE reserves in advance of their failure. Over 120+ clean independent audits and 120+ determinations of reasonable provision of loss and LAE reserves were issued from the inception date of each carrier through the year prior to failure.

To understand this anomaly, our internal due diligence went beyond financial information and the non-public information we received. Although all previously issued reports from third party professionals had noted nothing unusual, I suspected “something new, unknown and unidentified” was the proximate cause of the failures.

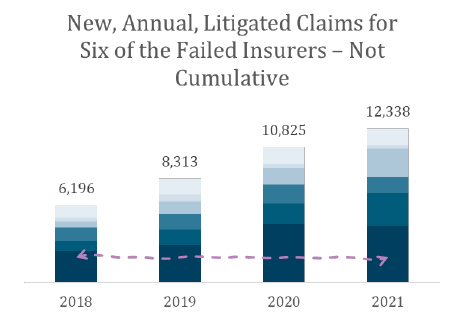

Service of Process Reports from the chief financial officer of Florida, https://apps.fldfs.com/LSOPReports/Reports/Report.aspx, provided insights. It was there that I found that these failed carriers, with an aggregate market share of three percent of residential homeowners’ insurance, had accumulated a market share of new, annual, litigated claims that grew from twice their level of market share at the end of 2018 to six times their market share at the end of 2021. Think about it: carriers with a 3 percent market share had accumulated 18 percent of newly reported litigated claims. I concluded that despite the level of disparate, disproportionate litigation associated with Florida’s homeowners’ insurance market “something new,” and as yet undetected, was in play.

The data referenced above is reduced to the graph below. When viewing the graph keep in mind:

• The count of litigated claims each year is NOT cumulative.

• The count excludes the non-litigated claims filed in the calendar year.

• A study by the State of Florida Office of Insurance Regulation determined that a litigated property insurance claim, peril for peril, costs 360 percent as much as a non-litigated claim; i.e., one litigated claim costs as much as (nearly) four non-litigated claims.

Recognizing that the level of the litigation dysfunction in the residential property insurance marketplace during this time period was well-documented, consistent, and known to all professionals, I suspected that “something new, unknown and as yet unidentified” was the proximate cause of the disparate increase in the number of new, annual litigated claims filed against these carriers vis a vis their market share. The fact that new, annual litigated claims had doubled in this brief time period implied to me that “technology” was a component of the “something new.”

Given the likelihood of “technology” as a component of the cause of the disparate increase in new, annual, litigated claim counts well in excess of the market share of the carriers, I turned to Todd Kozikowski, a data scientist with a strong information technology background as well as insurance experience. My ask was brief:

Within days of undertaking our project, Kozikowski unearthed the utilization of search engine optimization, pay-per-click advertising, sponsored ads, and other online tactics, supplemented by litigation marketing and litigation platforms, targeting insurers for the sole purpose of transitioning claims to contested or litigated status. Fortunately for the insurance industry and other targeted industries, Kozikowski leveraged his expertise and the findings of our research project to form 4WARN Inc., the first and only company of its kind, to assist targeted entities in mitigating the previously undetected, online threat that our research project unearthed.

Tech-Enabled Litigation Instigation Is Lethal and Lucrative

- The Business Model Can Destroy Carriers Through Industrial Scale Litigation

The business model has the ability to assess and exploit weaknesses in coverage and policy provisions at a technological, industrial scale never before attainable. Concurrently, the artificial intelligence litigation platforms underlying the business model have scaled the creation and filing of litigation to a level of economic feasibility that is in direct contrast to a defendant’s capability to respond. This is the case for insurers and transportation companies.

- The Business Model Has the Brute Power To Impact Claim Settlement Patterns

A review of the countrywide commercial automobile liability insurance claim data submitted by insurers reporting to the National Association of Insurance Companies at year-end 2014 provided insights on “claim transitioning” and claim settlement patterns. The analysis confirmed the capability of the business model of tech-enabled litigation instigation to transform claim settlement patterns over the past decade.

Over the period comprising accident years 2015 to 2024, claim settlement patterns have been demonstrably elongated as well as transitioned. The industry adage, “the longer it takes to settle a claim, the more expensive the claim will be,” rings true more than ever.

Prepared annually on a countrywide basis for all jurisdictions where an insurer is licensed, Schedule P, Part 1 C — Commercial Automobile Liability Insurance provides gross (direct and assumed), ceded, and net (gross minus ceded) premium, loss, and loss adjustment expense information by accident year, for the latest 10 accident years.

Also prepared annually on a countrywide basis is Schedule P, Part 5 C – Commercial Automobile Liability Insurance. This schedule provides the Cumulative Number of Claims Reported Direct and Assumed at Year-End, Number of Claims Outstanding Direct and Assumed at Year-End, and Cumulative Number of Claims Closed with Loss Payment Direct and Assumed at Year-End.

Using the claim counts in Schedule P, Part 5 C, one can estimate the Cumulative Number of Claims Closed Without Loss Payment Direct and Assumed at Year-End by calculating as follows:

Cumulative Number of Claims Reported Direct and Assumed Year-End

Minus Number of Claims Outstanding Direct and Assumed at Year-End

Minus Cumulative Number of Claims Closed with Loss Payment Direct and Assumed Year-End

Equals Cumulative Number of Claims Closed Without Loss Payment Direct and Assumed Year-End.

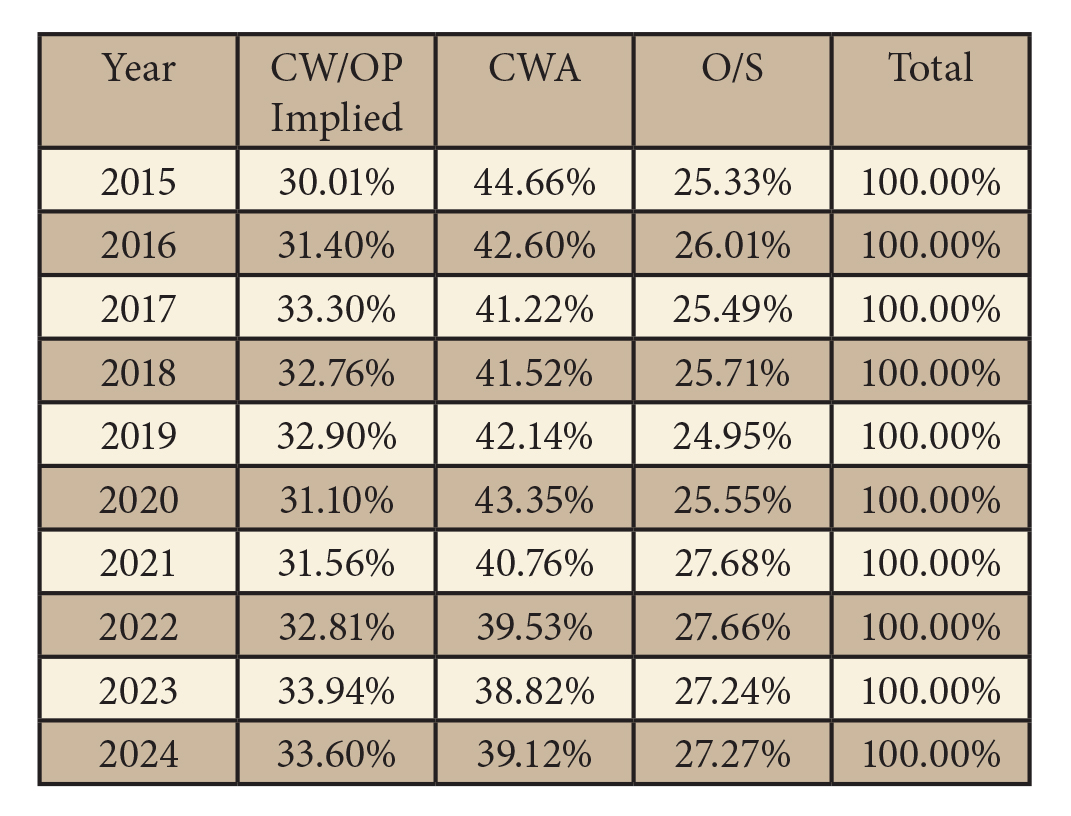

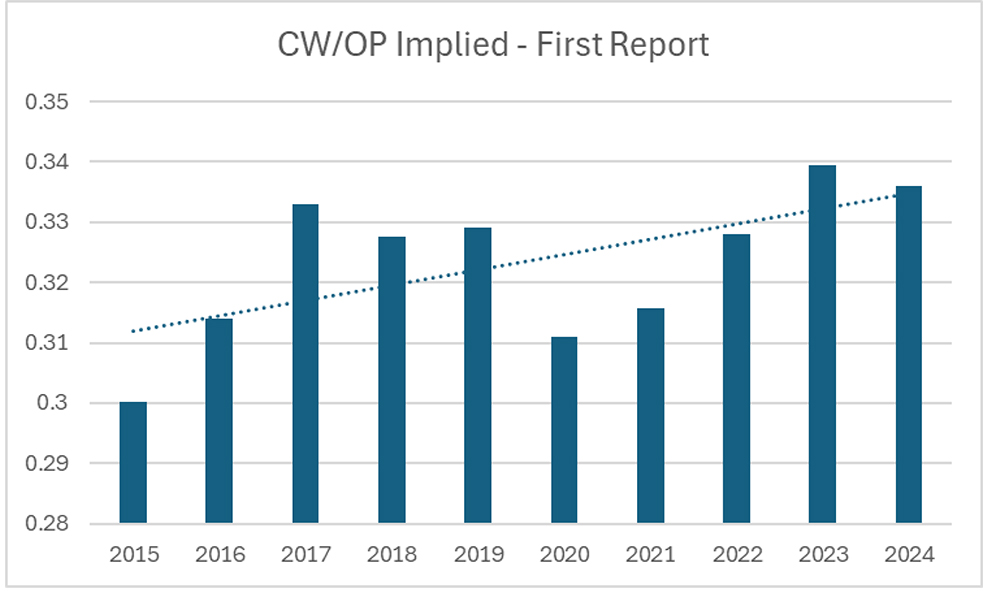

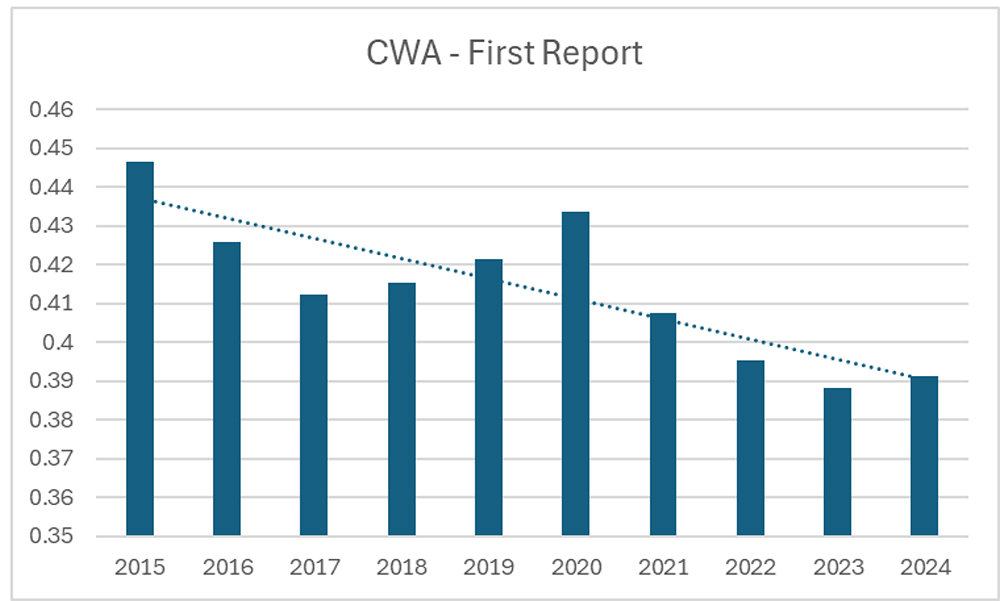

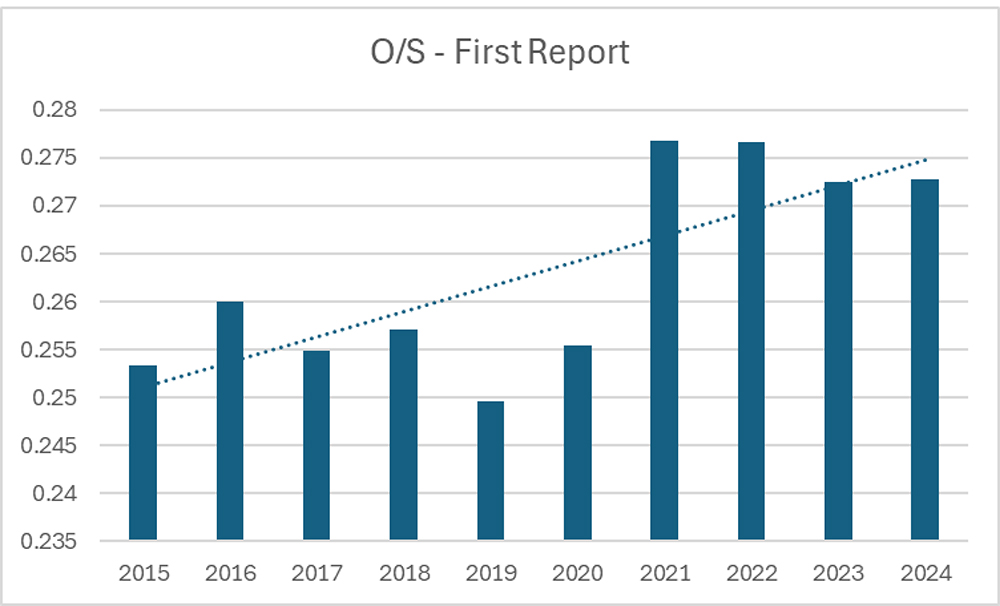

Using these three claim categories, and the claim counts at first report at each accident year-end, 2015 to 2024, the percentage of claims in each category for the latest ten accident years were:

The percentage of claims closed without payment, CW/OP Implied, has increased over time. In light of the discovery of the business model of tech-enabled litigation instigation and the scaling of the cost to file a contested or litigated claim via a litigation platform, we believe that the increasing percentage of claims transitioning to CW/OP implied is due, in large part, to the introduction of economies of scale. From this lower cost of filing suit emerged an incremental increase in the number of marginal claims presented to insurers. (Why not? It’s cheap).

Concurrently, given the increase in claims closed without a payment and the effort necessary to settle those claims, the percentage of claims closed with an amount at first report, CWA, declined markedly over the last 10 accident years. We believe that the concomitant transitioning of claims from CWA status to Outstanding status has been influenced by two major phenomena associated with the business model of tech-enabled litigation instigation. First, claim departments have had to expend their resources to respond to an increasing percentage of claims that were economical to present yet ultimately closed without payment, and second, more claims are being contested or litigated, which also leads to increases in the percentage of claims outstanding.

CW/OPs increase, CWAs decrease and the percentage of outstanding claims increases. Loss adjustment expenses also increase.

Given that the cost of a contested or litigated claim is a significant multiple of the cost of a policyholder reported claim, a modest increase in the percentage of claims outstanding will have a multiplier effect on the ultimate cost to defend and settle outstanding claims.

In summary, the online business model capable of devastating carriers and destroying the availability and affordability of insurance in entire markets was likely to have been in place since about 2017. Undetected until Demotech’s research project and the efforts of Todd Kozikowski, opportunists have been utilizing search engine optimization, pay-per-click advertising, and other online tactics to harness artificial intelligence platforms for the sole purpose of securing contested and litigated claims. Concurrently, litigation platforms have scaled the cost to file suit or contest claims, resulting in an increase in the percentage of claims closed without payment, which also served to elongate payment and settlement patterns.

Recapping thus far, we have:

• Familiarized you with Demotech’s research project, which was designed to identify the “something new” that destroyed carriers through disparate increases in their new, annual litigated claims.

• Advised you that Todd Kozikowski identified the “something new” as the covert business model of tech-enabled litigation instigation, and founded 4WARN Inc. to provide company-specific responses to remediate the impact of the targeting deployed via the online business model.

• Concurrently, using commercial automobile liability insurance as an illustration, we concurrently alert the transportation and logistics sector to the power and sophistication of the business model targeting them online.

Despite the insurance sector having 3 trillion dollars in admitted assets, and more than 1 trillion in direct premium written annually, the business model of tech-enabled litigation instigation demonstrated the ability to transition industry claim settlement patterns. This business model is well-entrenched, successful, and produces lucrative operating results.

The evidence of its efficacy is the attraction of third-party litigation funding capital by the billions. In addition to its financial results attracting third-party litigation funding by the billions, the success of the business model has emboldened plaintiff law firms to seek amendment to existing rules of professional conduct so as to allow non-lawyers to invest in, own, or coordinate the marketing activities of law firms, form alternate business structures, and implement managed services organizations.

- The Success of the Business Model Attracted the Attention of the Investment Community

This previously covert online business model was known by the legal and investment communities prior to our research unearthing it. The business model has the capability to destroy insurers, and transition claim settlement patterns. It has also contributed to the death of transportation companies, including but not limited to Yellow Freight, Davies Transportation, Carroll Fulmer, Celadon, NationWide, Preston, Transcon, Jevic, and Arrow.

The business model attracts third-party litigation funding by leveraging its sheer brute force. That power has encouraged some within the legal profession to embrace tech-enabled litigation instigation as an opportunity for expanding their law firms. In response to the wide-spread utilization of litigation funding, litigation funding has emerged as an asset class that Bloomberg rated as the top asset class with respect to annualized yield. Today, there are third party litigation funding sites that invite investments and also explore litigation investment opportunities.

Efforts focused on the disclosure of third-party litigation funding, enacted to date, and viewed as successful initiatives by some, have instead become templates for crafting contracts and funding relationships that need not be disclosed. In other words, once one knows what must be disclosed, one can craft agreements that circumvent disclosure. Disclosure is necessary but it is not sufficient.

- The Business Model Has Transformed the Legal Profession

Rule 5.4 of the American Bar Association Model Rules of Professional Conduct addresses the professional independence of law firms and associations:

Law Firms and Associations

(a) A lawyer or law firm shall not share legal fees with a nonlawyer, except that:

(1) an agreement by a lawyer with the lawyer’s firm, partner, or associate may provide for the payment of money, over a reasonable period after the lawyer’s death, to the lawyer’s estate or to one or more specified persons.

(2) a lawyer who purchases the practice of a deceased, disabled, or disappeared lawyer may, pursuant to the provisions of Rule 1.17, pay to the estate or other representative of that lawyer the agreed-upon

purchase price.

(3) a lawyer or law firm may include nonlawyer employees in a compensation or retirement plan, even though the plan is based in whole or in part on a profit-sharing arrangement; and

(4) a lawyer may share court-awarded legal fees with a nonprofit organization that employed, retained, or recommended employment of the lawyer in the matter.

(b) A lawyer shall not form a partnership with a nonlawyer if any of the activities of the partnership consist of the practice of law.

(c) A lawyer shall not permit a person who recommends, employs, or pays the lawyer to render legal services for another to direct or regulate the lawyer’s professional judgment in rendering such legal services.

(d) A lawyer shall not practice with or in the form of a professional corporation or association authorized to practice law for a profit, if:

(1) a nonlawyer owns any interest therein, except that a fiduciary representative of the estate of a lawyer may hold the stock or interest of the lawyer for a reasonable time during administration;

(2) a nonlawyer is a corporate director or officer thereof or occupies the position of similar responsibility in any form of association other than a corporation;

or (3) a nonlawyer has the right to direct or control the professional judgment of a lawyer.

Circa 2020, Utah, Arizona, and the District of Columbia amended their rules of professional conduct for lawyers to permit non-lawyers to have an interest in a professional corporation or association or to permit nonlawyers to hold positions of responsibility in such entities.

Further evidence of the transformation within the legal profession is the Association of Professional Responsibility Lawyers letter dated Dec. 12, 2024, to William R. Bay, president, American Bar Association. The correspondence and its supporting report discussed “a critical need for changes to this ethics rule to address the continued, inevitable involvement of non-lawyers in legal delivery systems while maintaining regulations that protect consumers. APRL’s Board of Directors, identified on this letterhead, voted unanimously to adopt the proposed revised rule, and authorized public dissemination of the Proposed Rule and Report.”

The APRL further noted, “The Report details the history of existing Rule 5.4, discusses the expressed and implied exceptions to the rule that presently exist, and explains how the current rule fails to address the contemporary and ever-evolving practice of law.”

The ABA has not amended Rule 5.4 of its Model Rules of Professional Conduct. The Commonwealth of Puerto Rico amended Rule 5.4 effective Jan. 1, 2026, to permit alternative business structures. In contrast, the state of California has preemptively denied non-lawyer owned law firms by passing AB 931, signed into law by Gov. Gavin Newsom.

Note that the development of artificial intelligence platforms and litigation marketing firms have also contributed to the transformation of the legal profession. Some on the plaintiff side have suggested that law firms should spend up to 20 percent of revenue on technology. Another commented that legal firms should transform themselves into technology firms.

Closing Thoughts on how a “Fair Share” Regulation Could Address the Challenge

Forward thinking organizations focused on consumer protection and the impact of fraud and opportunism, e.g., the Louisiana Department of Insurance, Coalition Against Insurance Fraud, and National Insurance Crime Bureau, to name a few, are familiar with the research project and accept the reality and existence of this online business model. But the online business model is actuated worldwide where no single regulator can fully address each facet of the business model.

In the insurance sector, tech-enabled litigation instigation has litigated carriers to death and demonstrated the capability to transition the claim settlement patterns of an entire industry. The financial impact of claim transitioning has also devastated the transportation sector. In the transportation and logistics sector, transportation carriers referenced litigation as a contributing factor to their failures; Celadon, Yellow Freight, NationWide, Davies, Preston, Transcon, Jevic, Arrow, and Caroll Fulmer, to name some.

The ruthless effectiveness of the business model has been rewarded with access to tens of billions in third party litigation funding as well as structural changes in rules of professional conduct for lawyers in some jurisdictions and the growth of managed services organizations within the legal community. The weaponization of fortuitous events is entrenched and well under way. What, if any, single regulator can slow down this effort?

Disclosures of litigation funding are viewed as a deterrent. However, to date, when disclosure of third-party litigation funding has been enacted into law, safe harbors emerged to shield categories of funding from disclosure. Similarly, investments made through alternate business structures and managed services organizations may not be required to file disclosures. The availability and affordability of insurance will remain problematic as long as online tech-enabled litigation instigation targets the insurance industry, ceteris paribus.

Given the overwhelming brute force of this business model, how might any regulator overseeing a component of this online business model reign in all of the numerous capabilities of the lucrative business model attracting tens of billions of dollars in third-party litigation funding? Sen. Thom Tillis of North Carolina and Rep. Kevin Hern of Oklahoma have proposed an effective first step: a uniform federal tax on net profits earned by third-party entities financing civil litigation.

A proposal to implement a uniform tax rate on the net profits from third-party litigation funding would reduce the attractiveness of investing in civil litigation yet continue to provide “the access to justice” that the litigation funders state that they provide. Absent action, third-party litigation funding is fueling an online business model that is detrimental to the insurance industry, and ultimately harmful to the stability of insurance markets and the businesses and consumers insurers support. Until the lucrative profits of the business model of tech-enabled litigation instigation are taxed consistently and appropriately, the business model will continue to evolve and expand. Litigation funding is not driving the bus; it is drafting behind a bus with unfettered speed and a clear path toward profitability.

Sen. Thom Tillis’ and Rep. Kevin Hern’s efforts to tax the profits emerging from third-party litigation funding are critical because the proposed legislation implicitly recognizes that the business model of tech-enabled litigation instigation is generating profits that attract the litigation funding. Creative structures and tax loopholes for third-party litigation funding have resulted in the evolution of a business model of unprecedented power and often untaxed profitability. Consistent taxation of the operating results of the business model will help level the playing field.

Stay informed with the Demotech Difference Magazine.